Real Estate Private Equity: Interview Guide (With Questions & Answers)

Get expert tips and sample real estate private equity interview questions—understand what firms look for and how to stand out in technical and fit rounds.

Posted August 10, 2025

Table of Contents

Breaking into real estate private equity is hard, not just because the roles are competitive, but because the interview process is opaque. Most candidates know to expect technical questions, but few realize how much firms care about how you think, how you communicate, and how you’d operate in the real world.

This guide breaks it all down. From mental math and underwriting prompts to deal walk-throughs and fit questions, we’ll show you what top firms are really looking for and how to stand out, no matter your background or role level.

Read: Private Equity Interviews: The Ultimate Guide

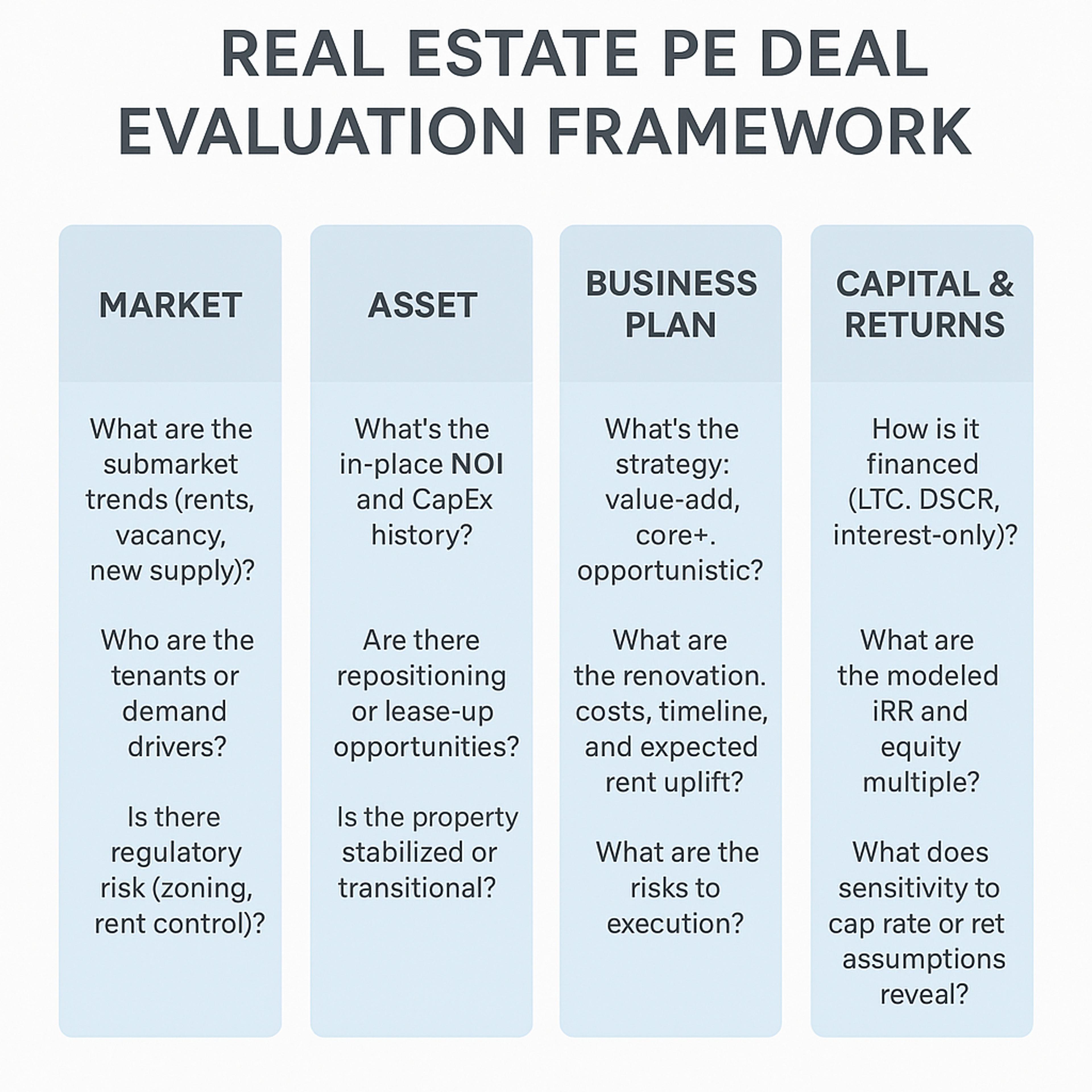

What Is a Real Estate Private Equity Interview Really Testing?

Real estate private equity (REPE) interviews are designed to test more than just your resume. Firms want to assess your ability to think like an investor, such as underwriting risk, evaluating returns, and communicating your thought process clearly.

Core Skills Firms Want to See

- Investment Thinking - Real estate private equity professionals must think like owners. Interviewers look for candidates who can identify promising investment opportunities, assess risk, and explain their rationale with clarity. It’s not enough to say a deal “looks good”. You need to articulate why it aligns with the firm’s return profile, capital structure, and investment strategy. Case questions like “Would you buy this at a 6% cap?” test whether you can break down tradeoffs and defend your assumptions.

- Market Judgment - REPE is a local game. Firms want candidates who understand the nuances of commercial real estate markets—not just broad economic trends. You’re expected to evaluate submarket fundamentals (rents, vacancy, absorption, comps), pinpoint supply/demand dynamics, and anticipate potential headwinds. In interviews, this often shows up in market memos or underwriting prompts where your answer hinges on your knowledge of the real estate industry at the block or asset level.

- Modeling Fluency - REPE roles require fluency, not just familiarity, with real estate financial modeling. You need to know how to build or manipulate models using metrics like NOI, DSCR, IRR, equity multiple, and cash flow. Interviewers expect you to move quickly in Excel, understand what drives returns, and spot red flags in assumptions. Modeling tests might ask you to adjust debt terms, tweak exit cap rates, or run sensitivity tables—all to assess how well you grasp the levers behind a deal’s performance.

- Communication - Clear, confident communication is non-negotiable. REPE professionals often present to investment committees, coordinate with management teams, or defend underwriting assumptions to skeptical partners. Firms are screening for candidates who can explain complex topics like a waterfall structure or market thesis in a way that’s logical, concise, and persuasive. Expect questions like “Tell me about a time you had to justify your decision.” They’re testing your ability to think on your feet and own your judgment.

Read: Top Skills You Need to Break Into Private Equity

What Makes REPE Different from Traditional PE Interviews

Unlike traditional private equity, REPE interviews focus more on asset-level risk and commercial real estate fundamentals than just capital structure gymnastics.

| Category | Traditional Private Equity (Corporate PE) | Real Estate Private Equity (REPE) |

|---|---|---|

| Primary Focus | Acquiring companies via leveraged buyouts (LBOs), optimizing capital structure, and driving operational improvement across industries | Acquiring, operating, and exiting real estate assets; heavy emphasis on asset-level performance, market selection, and downside risk mitigation |

| Deal Drivers | Revenue/margin expansion, cost synergies, multiple arbitrage, and exit timing | Rent growth, occupancy, lease structure, property repositioning, submarket dynamics |

| Key Metrics | IRR, MOIC, EBITDA, valuation multiples (EV/EBITDA), debt/EBITDA | Cap rates, Net Operating Income (NOI), Debt Service Coverage Ratio (DSCR), Equity Multiple, Unlevered/Levered IRR, cash-on-cash returns |

| Financial Modeling | 3-statement models, LBOs, accretion/dilution, sensitivity on exit multiples, and debt terms | Real estate financial modeling: buildout of cash flows by tenant/unit, debt modeling (LTC/LTV), waterfall structures, CapEx schedules, and IRR sensitivity to purchase price, exit cap, and stabilized property performance |

| Case Study Format | Full-blown LBO model and investment memo; may include comps analysis and industry deep dive | Asset underwriting with rent rolls, OMs, and market assumptions; write-up may include “Buy or Pass” decisions or market memo justifying entry cap rate and business plan |

| Assumptions Focus | Revenue CAGR, margin expansion, customer retention, valuation multiple at exit | Rent growth, vacancy, tenant rollover, operating expenses, capital expenditures, debt service, and exit cap rate compression or expansion |

| Due Diligence Scope | Analyze company financials, management team, industry trends, and competitive landscape | Evaluate property value, condition, sponsor track record, local market trends, zoning, lease terms, and property taxes |

| Team Interaction | Heavy focus on executive teams, consultants, and financial advisors | Interaction with property managers, developers, brokers, appraisers, and real estate operating companies |

| Interview Emphasis | Operational strategy, market sizing, 3-statement fluency, industry angles | Cap rate math, NOI underwriting, market selection, lease analysis, and demonstration of genuine interest in real assets |

Read: The Different Types of Private Equity — The Ultimate Guide

Interview Formats in Real Estate Private Equity

Expect a multi-stage process designed to test technical ability, commercial judgment, and cultural fit. Here’s what each round typically looks like—and how to prepare like a pro:

| Format | Duration | What Firms Are Testing | Expert Prep Tips |

|---|---|---|---|

| Phone Screens | 30–45 minutes | Quick assessment of your communication, motivation, and basic technical fluency. They want to see if you're sharp, articulate, and actually understand what REPE is. | Refine your “Why REPE” and “Why this firm” answers. Be ready to walk through your resume and talk through a deal or asset you’ve analyzed, even informally. Clarity and structure matter more than polish. |

| Technical Interviews | 1–2 hours | Tests your grasp of real estate finance, cash flow modeling, mental math, and understanding of key metrics (e.g., cap rates, IRR, DSCR). You may get verbal questions or Excel-based drills. | Brush up on real estate financial modeling—especially for multifamily and office buildings. Practice calculating net operating income, debt yield, and building a basic pro forma. Be ready to explain your logic step-by-step. Use real-world examples. |

| Case Studies | 1–3 hours or take-home | Simulates real work: underwriting a deal, writing an investment memo, or making a Buy/Pass decision. Firms evaluate how you think through potential investments, not just your model. | Practice underwriting live deals (LoopNet, OM packages) and writing short memos justifying your recommendation. Know how to analyze comps, rent rolls, and exit cap assumptions. Be structured—your memo should reflect an actual investment thesis. |

| Superdays | Half-day to full-day | Tests everything: technical skills, judgment, communication, stamina, and culture fit. Multiple rounds with junior and senior interviewers. | Be consistent across interviews. Build muscle memory for your deal walk-through, fit answers, and mental math. Research the firm’s portfolio companies, investment strategy, and recent deals to show tailored insight. Energy and composure matter—especially late in the day. |

Pro Tip: Most firms structure their interviews to see how you'd actually perform on the job. It’s less about getting every number perfect and more about how you think through real estate problems. Practice answering out loud, like you’re already part of the team.

Who This Interview Guide Is For (and What to Expect by Role Type)

Real estate private equity interviews are not one-size-fits-all. The expectations shift significantly based on your role level, background, and the type of firm you’re targeting. Whether you're a first-time analyst or a post-MBA lateral, preparing with the right lens is critical. Here's what to expect by path:

Analyst vs Associate vs Post-MBA Candidates

- Analyst candidates are expected to demonstrate strong technical foundations and the ability to execute quickly. While you won’t be leading deals, you will be responsible for underwriting, modeling, and supporting acquisition analysis. Interviews typically involve mental math drills, cap rate logic, and cash flow breakdowns, alongside questions that test whether you truly understand how value is created in real estate. What separates standout analysts is not just modeling skill, but their ability to articulate how those numbers tie to asset-level performance and investment return.

- Associates are judged not only on their technical fluency but also on their ability to think like investors. You’ll be expected to run models end-to-end, adjust assumptions with commercial intuition, and defend those assumptions to senior team members. Case studies may involve drafting a market memo, building a rent roll-based pro forma, or determining whether to pass or proceed on a deal based on nuanced underwriting. Firms are looking for confident communicators who can handle responsibility and begin to shape investment narratives.

Read: Analyst vs. Associate: Role, Responsibilities, & Salary

- Post-MBA candidates are evaluated at an entirely different altitude. At this level, your interviewers are looking for judgment, strategic thinking, and leadership potential. Expect to be pushed on investment theses, portfolio-level thinking, and your ability to make capital allocation decisions. You should be ready to talk through how you'd structure deals, evaluate risk/return, and influence investment committees. The bar is high: firms are hiring you to eventually originate, lead, and manage real estate investments—not just model them.

Post-MBA Insight: Your edge isn’t technical—it’s judgment. Be ready to articulate a clear investment thesis, compare deal structures, and speak to how you'd lead diligence.

Lateral vs Entry-Level Interviews

Lateral interviews tend to be more rigorous and deal-specific. Interviewers will dig into your actual experience, asking you to walk through real deals, explain where assumptions broke down, and assess how you’ve added value at your current or previous firm. Questions around portfolio company performance, lease-up execution, or asset repositioning are common. The best lateral candidates are clear on why they’re making a move and can articulate how they’ll strengthen the new firm’s bench, whether through sourcing, underwriting depth, or asset class knowledge.

Callout: Best for Lateral Interviews! Be ready to explain how your past deals performed vs. pro forma and how you'd improve underwriting on future assets.

In contrast, entry-level interviews focus on evaluating potential. You won’t be expected to have real-deal experience, but you will be expected to demonstrate a genuine interest in the real estate industry, strong technical preparation, and a thoughtful reason for pursuing REPE. A candidate who has built their own underwriting models, analyzed mock deals, or studied the local multifamily market on their own will immediately stand out. Demonstrated initiative and coachability are often more important than polish.

Callout: Strong Answer Starter - "I haven’t worked on a live deal yet, but I built a mock underwriting for a value-add multifamily property in Austin. Here’s how I approached it…”

REPE Internship Interviews: What’s Different?

Internship interviews are generally shorter but still revealing. Firms are looking for students who show curiosity, quick learning ability, and a basic grasp of commercial real estate fundamentals. You might be asked to walk through a hypothetical underwriting scenario, such as estimating a property’s value using cap rate math, or identifying value-add opportunities in a rent-stabilized asset. While modeling is rarely tested in-depth at this stage, understanding how net operating income, cap rates, and cash flow tie together is essential. Many firms use internship interviews as a filter for future full-time hires, so this is your chance to show both aptitude and long-term interest in the space.

Expert Tip: Practice underwriting 2–3 public listings (e.g. LoopNet) with back-of-the-envelope math. This signals initiative and real-world thinking.

Call out: Take Note, REPE Internship Applicants!

Cap rate math and NOI calculations are common screeners. Know how to backsolve property value or IRR using simple assumptions.

Read: Top Private Equity Internship Programs in 2025 (and How to Stand Out)

Institutional vs Smaller Sponsor Shops

Institutional real estate private equity firms, such as Blackstone, Brookfield, and Starwood, tend to have more formal, multi-round interview processes. These may include technical modeling tests, detailed case studies, and multiple rounds of behavioral and strategic interviews. The bar is higher across the board, but so is the clarity of expectations. Candidates should be prepared to analyze past deals the firm has done, speak to its investment strategy, and show how they’d fit into an already high-performing team. Demonstrating knowledge of the firm’s capital sources, such as pension funds or sovereign wealth vehicles, and how it raises and deploys capital is often a plus.

Smaller sponsor shops, on the other hand, may have fewer structured processes but a higher emphasis on real-world intuition and cultural fit. Interviews may feel more casual or entrepreneurial, but the expectations remain high. You might be asked how you’d underwrite a local asset with limited data, how you’d approach deal sourcing in a tight market, or how you’d manage relationships with leasing brokers or lenders. At these firms, real estate fluency often matters more than resume pedigree. Demonstrating hustle, local market knowledge, and a self-starter mentality can give you a real edge.

Read: The 5 Most Prestigious Private Equity Firms

Real Estate Private Equity Technical Interview Questions

Technical interviews in real estate private equity go beyond formulas—they test your ability to underwrite deals like an investor. Firms want to know: Do you understand how a property creates value, how risk flows through the capital stack, and how to translate assumptions into projected returns?

Here’s what top candidates master before stepping into the room:

Real Estate-Specific Accounting and Valuation

You’ll be expected to calculate and interpret the core metrics that drive investment decisions in commercial real estate. Knowing the formulas isn’t enough; interviewers are assessing whether you understand the logic behind them and how they interact in underwriting.

Net Operating Income (NOI) - The foundation of real estate valuation, NOI = Potential Gross Income – Vacancy – Operating Expenses. It excludes financing costs, depreciation, and taxes to reflect the property’s true operating performance. You’ll use NOI to derive cap rates, calculate DSCR, and evaluate cash flow available to equity holders.

Cap Rates - Cap Rate = NOI / Purchase Price. This is the industry’s shorthand for valuation and return expectations. A lower cap rate implies a higher valuation (and often lower perceived risk). Interviewers often test your ability to back-solve property value from cap rate assumptions or explain why a deal trades at a premium or discount.

DSCR (Debt Service Coverage Ratio) - DSCR = NOI / Annual Debt Service. This measures the asset’s ability to cover debt payments. A DSCR below 1.0 signals negative cash flow to the lender, often a deal-breaker. You may be asked to calculate DSCR under different loan-to-cost scenarios or explain how rising operating expenses could impact coverage.

IRR (Internal Rate of Return) - The IRR is the discount rate that makes the net present value (NPV) of future cash flows equal to zero. In REPE, both levered IRR (after debt) and unlevered IRR (before debt) matter, depending on your role in the capital structure. You’ll be expected to compute IRR manually or explain how holding period, leverage, and exit price affect it.

Levered vs. Unlevered Returns - Unlevered returns reflect the property’s performance independent of financing; levered returns incorporate the effects of debt service and magnify both upside and downside. Strong candidates can articulate when leverage is accretive—and when it introduces risk.

Take Note, Analyst and Internship Candidates: Be prepared to calculate these metrics quickly and explain what each one tells you about the deal’s quality and risk.

Market Assumptions & Underwriting Scenarios

REPE interviews often include case-style questions that test your ability to apply judgment—not just math. You might be asked something like:

“You’re evaluating a $25M multifamily asset in Dallas. Rents have grown 6% YoY, but concessions are rising. How do you underwrite rent growth and exit cap?”

To answer well, you need to show market intuition and back up your assumptions with real-world logic. Common levers include:

- Rent Growth Assumptions: Based on historicals, submarket comps, absorption rates, and economic indicators. Interviewers want to see you balance optimism with realism.

- Exit Cap Rates: Should typically be equal to or higher than your entry cap unless you’re repositioning the asset or anticipating compression. Know how a 50bps shift can affect returns.

- Vacancy and Credit Loss: A “stabilized” asset might still carry lease rollover or tenant risk—especially in office or retail properties.

- Operating Expenses and Property Taxes: These can escalate over the hold period, especially in value-add deals. Many candidates forget to model re-assessments or how firms raise capital expenditures.

Post-MBA Insight: Top firms look for candidates who can defend their assumptions with clarity (e.g., “I’m using a 3.5% rent growth assumption based on trailing five-year submarket trends and limited new supply.”)

Key Excel Modeling Tasks You Might Be Asked to Perform

Expect a hands-on test or verbal walk-through covering the most common modeling workflows in real estate private equity. These are often timed and focused more on logic than formatting.

Cash Flow Model Buildout

You may be asked to build a forward-looking cash flow projection using a rent roll, estimated expenses, and financing terms. You’ll need to structure your model so that NOI, debt service, and projected exit proceeds all flow logically into an IRR and equity multiple.

IRR and Equity Multiple Calculations

You’ll often be asked to calculate or interpret both. For example:

“If you invest $5M and receive $10M over 5 years, what’s your IRR and equity multiple?” Strong candidates can answer:

- Equity Multiple = 2.0x

- IRR ≈ 15%

Waterfall Modeling

In more advanced roles, you may need to build or explain a promote structure: how cash flows are split between LPs and GPs based on performance hurdles (e.g., 8% preferred return, 20% promote above a 12% IRR). You should understand how promotion structures impact total return and incentives.

Sensitivity Tables

Interviewers may ask you to run return sensitivities based on changes in purchase price, exit cap, or debt yield. Be able to interpret the results: How much does a 25bps increase in cap rate reduce equity IRR? How sensitive is your outcome to leverage?

Pro Tip: If they ask about cap rates, show you understand the relationship between property value, NOI, and market risk. For example:

“A 5% cap rate on $1M NOI implies a $20M property value. If the market softens, a 6% cap drops value to $16.7M—highlighting the sensitivity.”

Deal and Investment Case Questions in REPE Interviews

Case questions are central to assessing your judgment and real-world fluency.

“Walk Me Through a Deal” – Real Estate Edition

This is one of the most common—and telling—questions in any real estate private equity interview. Interviewers are assessing whether you can talk through a deal like an investor, not just recite facts from your resume. They're listening for structure, clarity, and commercial intuition.

A great answer should include the following elements:

- Deal Overview - Briefly describe the asset, location, deal size, and asset class. Be specific (e.g., “175-unit Class B multifamily in Charlotte’s South End submarket, acquired off-market for $32M”).

- Underwriting Assumptions - Share how you approached rent growth, vacancy, cap rate, and expenses. Highlight where you used third-party data (e.g., CoStar, broker opinions, tax records) to support your assumptions. Show you understand how levers affect NOI, cash flow, and risk.

- Capital Structure - Explain how the deal was financed (e.g., 65% LTC bridge loan at 6.5%, interest-only for 3 years) and why that structure fit the business plan. Mention any preferred equity, GP promote, or other waterfall elements.

- Value Creation Plan - What was the strategy? Renovations? Lease-up? Operational efficiency? Show your thought process around how the asset would outperform the market and what specific drivers (e.g., $150/unit rent bumps, re-tenanting retail) you underwrote.

- Exit Strategy - Tie your underwritten IRR and equity multiple to an expected hold period and exit cap rate. Explain sensitivities: “We underwrote a 5.25% exit cap but stressed to 5.75%, and still cleared a 17% IRR.”

- Your Role and Judgment - End with what you personally did and what you learned. The best candidates reflect on what they might have done differently or how the asset actually performed.

Pro Tip: Use a consistent framework for any deal discussion—even mock or hypothetical ones. Structure = confidence.

Case Study Formats: Market Memos, Buy vs. Pass Decisions

Most REPE firms will test how you approach a deal cold. These are designed to simulate the real investment process under time pressure. The goal is to assess your decision-making and communication skills, not just Excel chops.

Common formats include:

- Market Memo: “Summarize the opportunity, key risks, and recommendations in a 1-page memo.” Focus on clarity, logic, and investor-relevant insights—not fluffy market commentary.

- Buy vs. Pass: “Here’s a stabilized office deal in Atlanta. Would you buy at $28M with a 6.25% cap?” You'll need to analyze NOI, re-tenanting risk, capital expenditures, and potential upside or downside.

- Write-up with Model: You may be asked to submit a memo with a supporting Excel model. Some firms provide templates, others expect you to build from scratch.

Interviewers want to see if you can form a point of view, back it up with underwriting, and clearly communicate your recommendation. There’s rarely one “right” answer—but there is a right framework.

Sample Prompts: “Here’s a Multifamily Deal in Phoenix—What Would You Do?”

These mock scenarios are designed to reveal your thinking under pressure. Here’s an example you might get:

“Here’s a 240-unit Class B multifamily asset in Phoenix. Built in 1991, current rents are $1,350/month. Asking price is $39M, with in-place NOI of $2.6M. What do you think?”

Your response should hit:

- Valuation & Cap Rate - “That implies a 6.7% in-place cap. I’d want to confirm comps, but that’s in line with recent trades for stabilized product.”

- Business Plan - “Is there room for a light value-add? If market rents are $1,550, a $100/unit renovation could support rent bumps and improve NOI by $250K annually.”

- Risks - “Phoenix is a growth market, but has seen supply pressure. I’d want to check deliveries in the submarket and lease-up pace on nearby assets.”

- Financing - “We could underwrite with 65% LTC, fixed-rate debt, but I’d want to flex leverage depending on exit timing and interest rate environment.”

- Preliminary Decision - “Pending diligence, I’d explore a Buy at that price, assuming our underwritten exit cap and renovation budget hold.”

Analyst-Level Insight: Don’t try to memorize answers—practice breaking down deals logically. Interviewers want to hear how you think.

Red Flags Interviewers Look for in Deal Discussions

Even the best candidates lose ground when they gloss over details or show weak judgment. Common red flags include:

- Overly aggressive assumptions - Unrealistic rent growth, compression in exit cap rate, or underestimating operating expenses.

- Inconsistent math - Cap rate doesn’t align with NOI and purchase price; debt service doesn’t match stated DSCR.

- No clear business plan - Saying “value-add” without specifying what you're adding—how much renovation, what cost, and what impact on NOI?

- Lack of market context - Ignoring supply pipeline, tenant trends, or recent comps. If you're assuming rent growth, explain why it’s justified.

- Unaware of downside - Interviewers want you to surface risks, not hide them. Saying “it’s a great deal” without identifying what could go wrong is a miss.

Best candidates own their assumptions, defend their logic, and acknowledge the uncertainties. That’s what real investors do.

Behavioral and Fit Interview Questions (With Examples)

While technical skills get you through the door, fit and communication often determine who actually lands the offer. Real estate private equity teams are lean, high-stakes, and relationship-driven—so firms place huge weight on how you think, collaborate, and carry yourself.

These questions aren’t filler—they’re designed to assess how well you understand the REPE world, how you’ll perform under pressure, and whether you’ll be someone they trust in front of partners, lenders, and operating teams.

Each example below includes a strong and weak response, plus why it matters.

Why Real Estate Private Equity?

This is your chance to show that you’ve done the work, understand the asset class, and are driven by something deeper than a generic interest in “investing” or “tangible assets.”

Strong Answer: “I’m drawn to real estate private equity because it combines long-term, asset-level investing with operational complexity. During my internship at a commercial real estate brokerage, I realized I loved thinking about how small changes—like repositioning a tenant mix or reconfiguring floor plans can meaningfully shift NOI and property value. I want to work in a role where I’m underwriting real assets, building conviction in deals, and contributing to the full lifecycle of the private equity investment.”

Weak Answer: “I’ve always liked investing, and real estate is more stable than the stock market. Plus, I’ve heard the hours are better than traditional PE.”

Why It Matters: Firms are screening for genuine interest, not career arbitrage. They want to hire people who are excited about submarket research, lease assumptions, and figuring out how to turn a $40M property into a $55M exit, not someone who just wants to escape investment banking.

Why Our Firm / This Fund?

This question tests how well you understand the firm's investment strategy, market positioning, and portfolio. It's also a soft test of your commercial curiosity: Have you done the research to speak to what makes them different?

Strong Answer: “What stood out to me is your focus on infill industrial in Tier 2 markets, especially because that’s where I see the most mispricing right now. Your recent acquisition in Columbus, for example, showed a clear thesis around underutilized logistics assets with strong re-tenanting potential. I’m interested in firms that underwrite with discipline but still have conviction when others are sitting on the sidelines.”

Weak Answer: “I’ve heard great things about your culture, and I know you’re one of the top REPE firms. I just really want to learn.”

Why It Matters: This is about alignment. Firms want to know if you “get” what they do, and whether you’ll add value because you care about the same types of assets, strategies, and markets they do.

Tell Me About a Time You Missed a Detail or Had to Make a Judgment Call

This question tests self-awareness, maturity, and how you perform under uncertainty. In REPE, small errors in an Excel model or poor judgment on an underwriting assumption can cost millions.

Strong Answer: “At my internship, I was helping underwrite a multifamily deal and mistakenly used average asking rents instead of in-place rents from the T-12. This overstated NOI by about $200K. I caught the error during a review and immediately flagged it to the associate, along with the corrected pro forma. What I learned was the importance of reconciling data sources and always sense-checking assumptions, especially when they materially affect returns.”

Weak Answer: “I don’t really make mistakes; I tend to triple-check everything. I’m very detail-oriented.”

Why It Matters: REPE firms aren’t hiring perfection—they’re hiring people they trust to catch mistakes early, course-correct quickly, and take ownership. Your ability to reflect, communicate clearly, and learn from past errors is far more impressive than pretending you’ve never missed a detail.

Culture Fit: What Top Firms Are Screening For

This isn't about being “likable”. It’s about being dependable, coachable, and thoughtful. REPE teams are often small and execution-heavy. A junior hire who can communicate clearly, handle feedback well, and operate with sound judgment under pressure is invaluable.

Firms are looking for:

- Structured thinkers - Can you organize complex ideas and deliver insights without rambling?

- Clear communicators - Will you represent the firm well in meetings with partners, brokers, or lenders?

- High EQ operators - Can you collaborate with teams, manage deadlines, and handle tough feedback professionally?

- Ownership mindset - Do you treat every assignment—no matter how small—with care and accountability?

If you're interviewing at a fund where the team only has two associates and one VP overseeing a billion-dollar portfolio, they need to know they can trust you on live deals from day one.

Expert Tip: Practice your behavioral answers out loud. Great content falls flat when delivered nervously, and great delivery can elevate even a simple story. Interviewers are hiring future teammates—not just finance robots.

Mental Math & Modeling Questions You Should Expect

REPE mental math tests often trip up candidates from traditional finance backgrounds.

Common REPE Math Prompts

Real estate private equity interviews often include fast-paced mental math to assess whether you can think like an investor without relying on Excel. These prompts are rarely complex—they're designed to test your fluency with fundamental math and your ability to estimate under pressure.

The most common type is the cap rate valuation. For example, “If a property generates $1.2M in NOI and trades at a 6% cap rate, what’s the implied value?” You should be able to instantly answer: $20M. From there, expect quick follow-ups: “What if expenses increase by $100K?” or “What if the market softens to a 6.5% cap?”

You may also get back-solve prompts like, “What exit price is required to hit a 2x equity multiple over five years?” or “What’s the implied IRR on a $5M private equity investment that returns $10M in four years?” These test your sense of how cash flow timing and compounding interact. The ability to approximate quickly while explaining your logic is often more important than the exact number.

Short Modeling Tests You May Be Given

In addition to mental math, many firms administer a short modeling test—either in person or take-home. These are designed to replicate the kinds of tasks you’d perform on the job: building or reviewing a cash flow model, running sensitivities, or stress-testing assumptions.

You may be asked to build a simple pro forma from scratch using a rent roll and operating assumptions. In-place NOI, property taxes, capital expenditures, and debt service should flow logically to your final return outputs, typically IRR and equity multiple. More advanced roles may also include a basic waterfall model or promote structure.

The modeling is rarely complex, but interviewers are testing whether you understand what drives the deal, not just how to plug numbers into cells. If your cap rate, exit value, or loan sizing doesn’t match your assumptions, they’ll notice. They’re also evaluating how cleanly you present your model, how you prioritize accuracy, and how you respond under time pressure.

How to Practice for On-the-Fly Underwriting

Strong candidates don’t just memorize formulas—they build judgment by practicing with real deals. One of the most effective prep methods is to underwrite listings from LoopNet or offering memorandums. Take a live multifamily or industrial deal, extract rent roll data, estimate NOI, apply market cap rates, and test different capital structures. Then write out a one-paragraph investment thesis: Would you buy this asset? Why or why not?

Practicing this way sharpens your instincts around key levers: what makes a deal attractive, what assumptions are aggressive, and how small changes affect IRR or downside protection. It also forces you to think in investor language—something that sets apart candidates in interviews. Being able to walk through a deal without touching Excel is one of the clearest signs you’re ready for the job.

Another valuable approach is to build your own library of mental math exercises. Keep a running list of questions like “What’s the property value at a 5.75% cap on $850K NOI?” or “What DSCR does this loan structure imply?” Practice until your answers feel intuitive and your explanations are crisp.

Estimation Questions

Estimation questions are a high-leverage way to assess your deal sense. They typically take the form of: “If you invest $10M and double your money in four years, what’s the IRR?” The answer is roughly 18–20%. But more than the number, interviewers are looking at how you approach the question. Do you panic and start guessing? Or do you calmly explain your logic and walk them through your math?

Other examples include: “If you reduce operating expenses by $250K on a 5% cap rate asset, how much value did you create?” That answer is $5M. Candidates who can make that connection in real time, cash flow to value, are far more likely to move forward.

These questions aren’t about precision. They’re about commercial fluency, composure, and understanding how real estate math reflects real-world outcomes.

10 Common REPE Mental Math Questions (With Answers)

| Question | Expected Answer |

|---|---|

| A property generates $1.5M in NOI and trades at a 6% cap rate. What’s the value? | $25M |

| What’s the IRR on a 2x equity multiple over 4 years? | ~19% |

| NOI increases by $200K. What’s the value impact at a 5.5% cap rate? | ~$3.64M |

| You invest $4M and receive $8M after 5 years. What’s the IRR? | ~15% |

| Debt service is $1.2M and NOI is $1.8M. What’s the DSCR? | 1.5x |

| A $20M asset is purchased with 65% LTV. What’s the equity invested? | $7M |

| Operating expenses increase by $100K. How does that affect value at a 6.25% cap? | Value drops ~$1.6M |

| Rent increases $75/unit/month across 200 units. What’s the annualized NOI increase? | $180K |

| What’s the property value of $950K NOI at a 5.25% cap rate? | ~$18.1M |

| What’s the equity multiple if you invest $6M and receive $9M total? | 1.5x |

Need Expert Help on Real Estate Private Equity Interviews?

Breaking into real estate private equity is competitive—and most candidates don’t fail because they lack potential. They fall short because they haven’t been coached on how to think and communicate like an investor. That’s where we come in.

Top private equity coaches have sat on the other side of the table. They’ve worked at top REPE firms, led interviews, and evaluated candidates across all levels—from undergrad interns to post-MBA associates. They know exactly what top-performing candidates do differently, and they’ll help you get there. Browse PE coaches here.

See: The 10 Best Private Equity Career Coaches for Interview Prep & Training

Top Coaches

Read these next:

- 20+ Second-Round Interview Questions You Need to Know

- The 10 Best Questions to Ask Your Interviewer in a Private Equity Interview

- The 50 Most Common Private Equity Interview Questions

- The Best Venture Capital & Private Equity Newsletters and Podcasts

- Finance Internships for College & High School Students

FAQs

What’s the best way to talk through a real estate deal in an interview?

- Use a structured format: market → asset → underwriting → risks → outcome. Be specific and quantify where possible.

How important is real estate-specific modeling in REPE interviews?

- Very. Understanding NOI, DSCR, cap rates, and waterfalls is critical.

Why do firms ask mental math questions in real estate PE interviews?

- To test your fluency with real estate metrics and ability to think under pressure, like quickly calculating the cap rate for a property value.

What are the most common real estate private equity technical questions?

- NOI, cap rates, IRR, exit values, underwriting assumptions, capital structure, and Excel modeling tasks.

Is prior real estate experience required to break into REPE?

- Not always, but real estate financial modeling and a strong understanding of the real estate industry are essential. Some firms will train for skills, but not for passion.